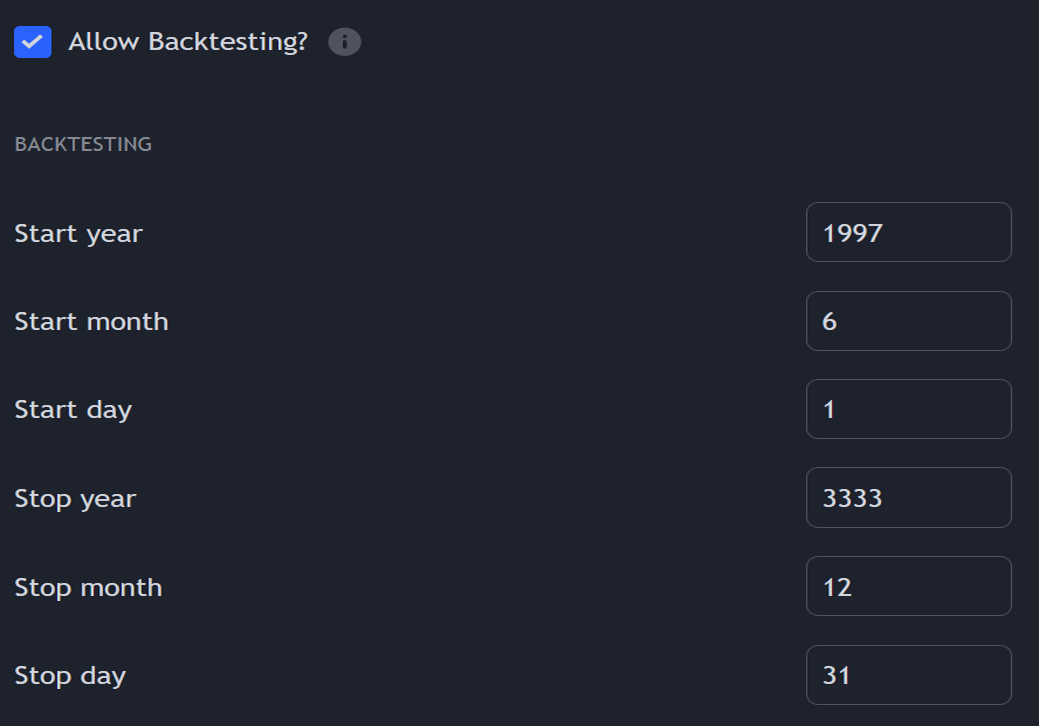

Backtesting

Historical Performance

Adjust the periods for backtesting to analyze the script's historical performance and trades during different timeframes.

You can turn backtesting on and off. This will disable signals all-together.

There are options to:

- Input a start day, month and year.

- Input an end day, month and year

All signals outside of the provided time range will be disregarded when building the historical backtesting report.

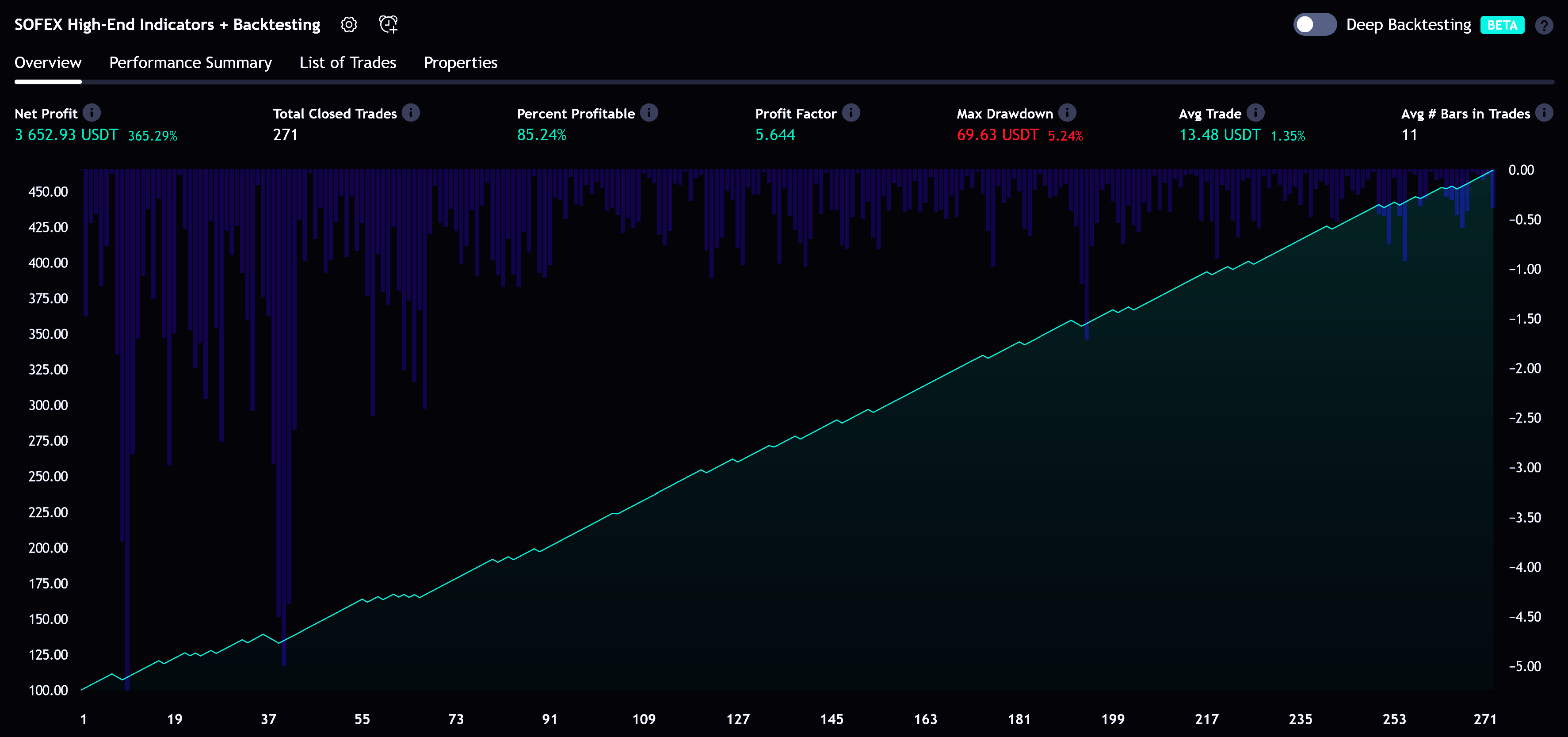

This is an example configuration of the system for BTCUSDT on Binance.

Hypothetical or simulated performance results have certain limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not been executed, the results may have under-or-over compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profit or losses similar to those shown.